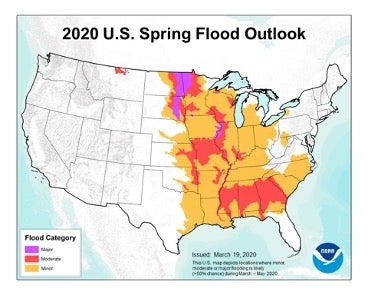

According to the spring flood outlook released by the National Oceanic and Atmospheric Association (NOAA), a third of the United States is at risk of inland flooding this spring – that’s roughly 1.26 million square miles, covering 23 states and affecting almost 130 million Americans (Cappucci). Spring floods in the U.S. are often brought on by snowmelt, ice jams, and thunderstorms. Intuitively these make sense as drivers: warmer temperatures lead to snowmelt and river thaws in the North, producing a lot of runoff in a short period of time, while thunderstorms occur frequently across Central and Eastern regions bringing intense rainfall that can generate flash flooding.

While not as severe as 2019, NOAA does expect this season to be above average in temperature and precipitation across the central and eastern portions of the country (NOAA). A number of areas are heading into the spring flood season well ahead on rainfall and snowpack, leading to saturated soils that will have a tougher time handling the downpours that can occur.

Snowmelt could negatively impact agriculture again in the Midwest and Northern regions by delaying planting. In these regions, major flooding is forecasted along sections of the Missouri River, Mississippi River, and the Red River of the North, with the Dakotas and Minnesota projected to be most impacted. The Southeast is also particularly vulnerable as the 2019-2020 meteorological winter was among the top five wettest on record. This has left many cities with saturated soils after having close to 30 inches of rain since the start of the year, and as a result, the& NOAA is forecasting moderate flooding over larger areas of Mississippi, Alabama and Georgia (Cappucci).

Image Source: NOAA

What will the summer and the rest of the year bring?

In addition to the usual considerations of rainfall and snowmelt, a number of less obvious but very important additional factors need to be taken into account. First of all, we need to consider antecedent conditions. For example, if areas prone to hurricanes and tropical storms get a lot of rainfall and melt in the spring, the saturated soil will not be able to absorb the heavy rainfall produced by tropical weather systems, as we saw with Florence (2018) in the Carolinas. Related to this is the impact of consecutive events: even relatively minor events can exacerbate future flooding if they occur in close proximity.

Therefore, as we approach the hurricane season, it is critical to consider flood from all sources, i.e., from tropical, extra-tropical, and convective weather systems, and the potential impacts of previous events.

Secondly, we must consider the impact of flood defenses and mitigation efforts (e.g., levees, diversion channels, dams/reservoirs, etc.). The U.S. river network is estimated to be protected by over 100,000 miles of defenses (USACE) which can mean the difference between a defended flood event or a flood that could cause a serious loss. The latter could be due to a lack of defenses or due to defense failure, as we saw in the Midwest 2019 floods.

However, only about 15-20% of these defenses are publicly documented and even less have information on their level of protection or current condition. As summer stretches into autumn and winter, one factor will become clear: flood defenses matter when it comes to underwriting and managing flood risk. Modeling flood risk without a complete view of flood mitigation measures can bias modeled losses, potentially leading to overly conservative views of flood risk and an inefficient use of capital. Having comprehensive defense information, as well as the ability to quantify sensitivities and impacts of various flood mitigation efforts and failure scenarios, facilitates appropriate flood risk selection, pricing, and portfolio growth decisions.

A model for all seasons!

Regardless of the season, the flood market in the U.S. continues to grow and evolve. How can you confidently underwrite risk in such a varied market for such a spatially high-resolution and temporally complex peril? It may seem obvious – you need a solution that is fit for purpose.

The U.S. Inland Flood HD model is such a solution. It has a long temporal simulation (50,000 years) that generates over 1 million flood events that provide a complete characterization of low- and high-severity events while accounting for event clustering, antecedent conditions, and seasonality. It captures temporal and spatial correlations of flood from all sources—tropical, extra-tropical, and convective weather systems—maintaining a “memory” of events in time and space to ensure preconditions impact subsequent events (e.g., consistent heavy rainfall in spring saturates soil, worsening potential flood extents and depths in summer/fall). And critically, the model not only includes a probabilistic defense model across the entire river network, but also allows defense customization to generate bespoke views and conduct sensitivity analyses enabling competitive pricing.

Because the model has such a large event set, it properly captures a rich set of possible tail events, minimizes what we term “model error” (ensuring loss convergence at fine scales and more accurately representing “reality”), and thus, avoids underestimation of risk. Surprise losses in the tail are the nightmare of any CRO, CUO or CFO, and can have serious financial consequences ranging from the need to purchase additional reinsurance cover to risk of ruin!

Implications for insurance

Although this season may not be as severe as last year’s, there may still be significant events causing substantial damage and loss. For those needing or seeking insurance, a large flood insurance gap remains. The highest flood insurance penetration is along the coast and major rivers in Special Flood Hazard Areas (i.e., flood zone groups A and V) designated by FEMA Federal Insurance Rate Maps (FIRMs); however, flooding often occurs outside these areas, which leads to sizeable uninsured losses.

Last spring, the Congressional Budget Office conducted a study using the RMS U.S. hurricane and flood models to estimate the expected cost of damage from hurricane wind and storm related-flooding along with data from the Federal Emergency Management Agency, the Department of Housing and Urban Development, the Small Business Administration, and the Office of Management and Budget. They found that of the $20 billion estimated annual residential flood losses (inland and coastal), roughly two-thirds are left uncompensated (CBO).

There has been a lot of discussion on how the FEMA FIRMs are outdated and have led to National Flood Insurance Program (NFIP) rates that are not adequately priced to the actual risk. However, the NFIP and FEMA are working to improve the rates in Risk Rating 2.0 with the help of catastrophe model vendors, including RMS.

The RMS U.S. Inland Flood HD Model and associated data products [U.S. Flood Depth Data, Susceptibility Data, Loss Costs, and Risk Scores] can help assess the current flood risk landscape at a granular resolution, providing the necessary insights to grow the flood insurance market and fill the protection gap. Having a thorough understanding of the underlying flood risk can assist in developing new products with appropriate pricing and underwriting guidelines, making sound decisions on growing portfolios with superior risk selection, and responsibly managing those portfolios in the context of your broader business.

Join us at Exceedance 2020 Virtual!

To learn more about the RMS U.S. Inland Flood HD Model and how it leverages the latest modeling science and technology to provide a comprehensive flood solution, be sure to attend Exceedance 2020 and join the session “Leveraging HD Capabilities to Understand Inland Flood Risk” Tuesday, May 5 at 12:30pm EDT, or join us in the Expert Bar to get your detailed flood questions answered.

U.S. Army Corps of Engineers, USACE. “National Levee Safety: About Levees.” USACE Headquarters, https://www.usace.army.mil/National-Levee-Safety/About-Levees/. Accessed 27 April 2020.

Share:

You May Also Like

June 27, 2019

An Award-Winning U.S. Inland Flood Model

It was off to London’s Savoy Hotel for members of the RMS London team last Thursday, for the Eleventh Trading Risk Awards. And apart from the great hospitality, and the flowing conversation from colleagues and industry peers alike, RMS was also recognized by the award judges, receiving the “Initiative of the Year” award for the RMS U.S. Inland Flood HD model.

Without sounding like an Oscar acceptance speech, on behalf of the team that worked on the model, I would like to thank the judging panel made up of representatives from the media and the industry for selecting our entry. Released last October, the flood model is designed to help the private insurance market seize the opportunities presented by this peril, and to also ultimately help accelerate flood insurance take up in the U.S.

Ben Brookes, managing director – capital and resilience solutions, RMS, (pictured center) receives the “Initiative of the Year” award at the Trading Risk Awards 2019In a country where hurricanes, tornados and wildfires can dominate the headlines, it is flood that is the most frequent and widespread peril in the U.S. Events range from small, localized flooding to widespread inundation impacting multiple river catchments and basins. The state-backed National Insurance Flood Program (NFIP) – recently extended until the end of September by Congress, dominates the flood insurance market, providing 95 percent of residential flood policies.

Even after significant flood events, such as from Hurricane Harvey in 2017, and Florence in 2018, NFIP policy numbers have recently plateaued; the New York Times reports that policies in force are below those a decade ago. In Midwest states, NFIP policies are down by a third since 2011, which has left many uninsured against this year’s ongoing flooding across the region. Flood is underinsured throughout much of the country, where only a third of homes in floodplains have insurance. And of the tens of trillions of dollars exposed to flood, still only a fraction is covered by the private market.

With FEMA looking to boost the number of households with flood insurance in the U.S from around five million now to eight million in 2022, what can be done to start to increase flood insurance penetration and to close this growing protection gap? How can private insurers enter the market with confidence and build a flood insurance business which will be profitable and sustainable in the long-term?

It is our belief that the insurance industry is currently inadequately served in terms of the accuracy and breadth of data available to achieve this task. As well as accessing accurate flood hazard data, this also extends to data on flood defenses, the first-floor height of a building or the presence of a basement – all key factors in assessing flood risk. There is also a need to use tools that can discern the high-gradient nature of flood extent and severity – and to accurately quantify probabilistic loss to exposures at risk.

We believe that the RMS U.S. Inland Flood HD Model does offer a comprehensive and well-validated view of flood risk throughout the contiguous U.S., which can help (re)insurers gain the necessary insights into the range of potential commercial opportunities associated with the private flood market. It captures the risk associated with all aspects of precipitation-induced flooding, including those resulting from tropical cyclone and non-tropical cyclone rainfall, while also accounting for factors that impact rainfall runoff (e.g., groundwater response, surface evapotranspiration, and snowmelt).

To capture flooding caused by tropical cyclones, the model is explicitly coupled to the same event set as the market-leading RMS North Atlantic Hurricane Model. Understanding flood risk and how it is correlated with wind exposure, is required for management of an overall book, risk tolerance and accumulations. And thus, it is particularly important to use a consistent view of risk across those aspects and across perils. By linking these models, it has enhanced the development of a truly complete and consistent view of the U.S. flood risk landscape – providing knowledge of how flood is spatially and temporally correlated across all its major sources, including storm surge and the wind peril.

Probabilistic modeling is essential, and the proprietary modeling methodology simulates over one million individual events, collectively representing 50,000 years of continuous precipitation, runoff, river discharge, and inundation within and across affected regions. These robust simulations provide a complete characterization of low- and high-severity flood events that could damage property, minimizing uncertainty to inform confident capital allocation, solvency assessments, and pricing based on model output. The model includes simulations of physically plausible flood events capable of causing losses far greater than have been observed historically, allowing (re)insurers to prepare for the potential financial impacts of the next flood catastrophe.

Using Innovative Modeling to Fill Critical Data Gaps

Flood hazard, vulnerability, and loss are extremely sensitive to building elevation and the presence of basements, which vary geographically across the U.S. When this data is not captured by the user, the model leverages proprietary inventory databases developed from extensive research to infer each building’s first floor height and basement likelihood. The explicit modeling of these two flood-specific characteristics, in addition to other general characteristics (e.g., construction class, occupancy, year built, etc.), helps reduce uncertainty in technical pricing with high-precision, per-location risk assessment.

Effective flood defenses also make a crucial difference when assessing flood risk. A major task of the RMS flood modeling team was to take disparate public levee data, which only accounts for a maximum of 20 percent of the nation’s flood defenses, together with the use of a proprietary stochastic modeling technique that accounts for the likely presence and standard of protection of defenses along the entire modeled river network.

This gives the option to see defended and undefended views of risk – to establish how the risk is reduced by a flood defense, and also allows users to customize these views, by adding their own defense information or adjusting the model’s default view. Allowing the market to quantify the sensitivities and impacts of various flood mitigation efforts and failure scenarios helps facilitate appropriate flood risk selection, pricing, and portfolio growth decisions throughout the U.S.

Gaining confidence and understanding around U.S. flood risk is a sound first step for the insurance industry to move forward and offer innovative coverages to meet the diverse needs of the market. And as the judging panel recognized, the U.S. Inland Flood Model represents real innovation to help achieve this.…

Dr. Holly Widen is a Product Manager in the Model Product Management team, focusing on the U.S. Flood suite of products. She joined RMS in 2016 upon completion of her Doctorate in Geography from Florida State University, where she studied tornado risk and vulnerability using applied spatial statistics. She has co-authored over ten peer-reviewed journal articles and is a member of the American Meteorological Society and the American Association of Geographers.