It has been reported that the current Ebola Virus Disease (EVD) epidemic, which has caused over 1,300 confirmed deaths in the Democratic Republic of the Congo (DRC) since its onset in August 2018, has now also caused at least one confirmed death in neighbouring Uganda.

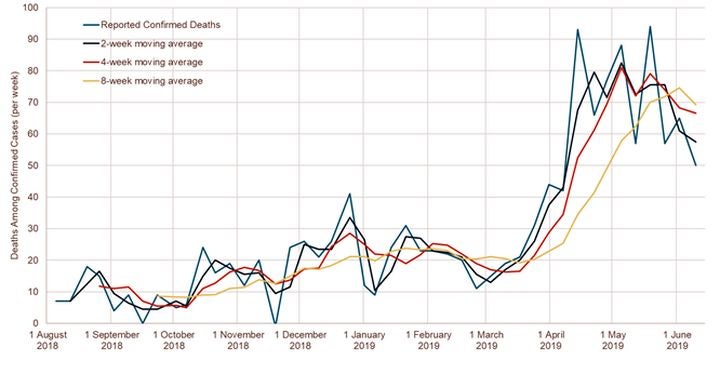

The number of confirmed deaths has been steadily increasing since the onset of the outbreak, though since March there has been a notable increase in the reported number of deaths per week. A recent trend shows a slight decrease from the peak, with the current situation report recording 50 deaths among confirmed EVD cases in the past week (Figure 1 below).

FIGURE 1. REPORTED CONFIRMED EVD DEATHS (PER WEEK) – SHOWING REPORTED WEEKLY DATA, AND FOR A RANGE OF MOVING TIME-AVERAGES (SOURCE: WHO).

The situation in DRC is complex; response efforts have been challenged by attacks on local health workers. David Gressly, UN Emergency Ebola Response Coordinator (EERC), recently commented on the difficulties faced. “The Ebola response is working in an operating environment of unprecedented complexity for a public health emergency – insecurity and political protests have led to periodic disruptions in our efforts to fight the disease.”

Despite the scale of the epidemic, and the local challenges in managing the outbreak, cases of EVD had until now been contained within the DRC.

It is understood that the first case of EVD in Uganda occurred as a result of a family attending the funeral of a relative in the DRC, where it is believed a five-year old child contracted the virus before returning to Uganda, where health workers identified the illness as EVD. Sadly, the child has now died, and a number of family members have also contracted EVD and are being treated.

Response

The 2014-2016 EVD epidemic resulted in more than 10,000 deaths across Sierra Leone, Liberia and Guinea. Since then, there have been two major advances in planned responses to similar outbreaks.

The epidemic accelerated efforts to search for an effective vaccine – funds were mobilized, and clinical trials were launched and completed in record time. Among more than seven candidate vaccines that have been tested, a “Recombinant Vesicular Stomatitis Virus Ebola Vaccine” (rVSV-ZEBOV) provided the most promising results with reported efficacy of 100 percent (95 percent confidence interval of 68.9 to 100 percent) among 2,119 vaccinated contacts in Guinea.

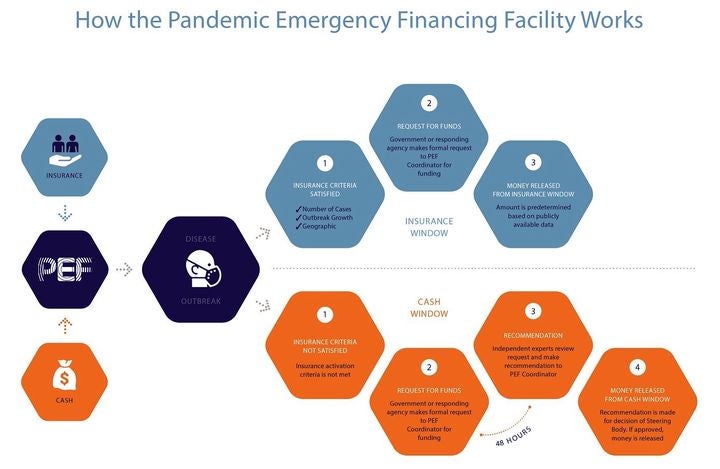

The World Bank developed the Pandemic Emergency Financing Facility (PEF) – a quick-disbursing financing mechanism that provides a surge of funds to enable a rapid and effective response to a large-scale disease outbreak. The PEF combines a ‘cash window’ with an ‘insurance window’ to provide funding to support outbreak management (Figure 2). A portion of the finance for the insurance window is sourced from the capital markets through a parametric catastrophe bond – the IBRD notes

FIGURE 2. WORLD BANK PANDEMIC EMERGENCY FINANCING FACILITY (PEF). AN OVERVIEW OF THE STRUCTURE, INCLUDING CASH WINDOW AND INSURANCE WINDOW COMPONENTS (SOURCE: WB).

Since the onset of the epidemic, a total of US$32 million has already been disbursed from the cash window, which is the flexible component of the PEF, where funds are disbursed based on agreement by a steering body.

There are more stringent rules attached to the insurance window – a set of predetermined criteria must be satisfied to determine if funds are released from the catastrophe bond. This structure is called a parametric trigger mechanism, it is required because the funds which support the insurance window are sourced from (re)insurance and capital markets, so a clear and pre-agreed objective process is required.

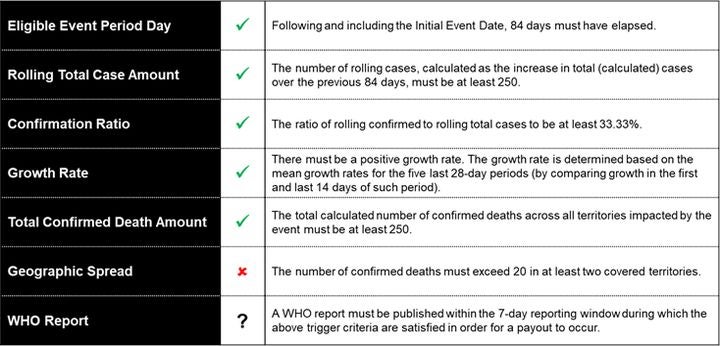

Due to the complex nature of epidemics, the parametric trigger mechanism has a range of dependent criteria which must all be satisfied before a payout can be authorized (Figure 3 below).

FIGURE 3. SUMMARY OF CATASTROPHE BOND TRIGGER CRITERIA (SOURCE: RMS VIA PUBLIC OFFERING MATERIALS).

Based on the current reported number of confirmed deaths, the structure would appear poised to make an initial payout, which would supply the PEF funds for disbursement to local governments and responding agencies.

However, there are additional criteria which must be met before this can happen. These criteria relate to the growth rate of the outbreak, and the geographic distribution of confirmed deaths. RMS does not have access to the detailed calculation procedures in the Calculation Agent Agreement. But according to preliminary RMS calculations, which are based only on publicly available WHO data, and the calculation procedure outlined in the cat bond offering materials which are made public on the World Bank data portal, the growth rate criteria could have been met.

The spread of the outbreak to Uganda therefore marks a notable incident with respect to the funds that may become available to support local response efforts. If the outbreak is not contained, and 20 confirmed EVD deaths occur in Uganda, then, subject to independent review and confirmation by the calculation agent, the bond may make a first payout to the PEF.

A Complex Issue

This type of structure, where multi-million dollar transfers are made based on reported deaths, growth rate and geographic criteria, obviously raises questions among those who view it for the first time.

However, it is important to recognize that the pre-agreed structure has been designed to explicitly address this type of complex crisis. The cash window of the PEF exists so that the facility has flexibility in its response, to ensure that some funds are available to assist with “severe single-country outbreaks”. The PEF insurance window exists to provide financial support for severe outbreaks which impact across multiple countries.

It is also important to recognize that, as with any complex crisis, finance is only one part of the solution. The local response systems are what will ultimately manage the epidemic. If the local responders are sufficiently supported with resources, including vaccines, medical expertise, and appropriate funding, then hopefully this crisis can be ended sooner.

Share:

You May Also Like

December 04, 2018

The Sum of Its Parts: Wildfire in Multi-Peril Catastrophe Bonds

When catastrophe strikes, it is not unusual for the insurance payout to differ from the policyholder’s expectation. The possibility of such a discrepancy is referred to as “basis risk”. The term, however, can be ill-defined and easily misunderstood.

Therein lies the problem, without definition it is easy for the basis risk associated with a structure to remain unidentified and unquantified. If left unspoken, basis risk can lead to problems down the line, when events do occur. So, as a starting point, we can most simply define basis risk as the “difference between expectation and outcome”.

Parametric insurance is most commonly associated with basis risk, though when defined like this, it becomes clear that basis risk exists within all insurance structures.

For indemnity insurance, basis risk could stem from the possibility that a contract fails to pay because of a legal miswording; for a modeled loss trigger, the difference between modeled loss and measured loss after an event; and for pure parametric insurance, the difference between the index loss calculated from a wind speed measurement and the total actual loss.

The primary drivers of basis risk vary between structures. To quantify basis risk, it is first necessary to identify the primary sources of uncertainty with respect to each structure. Once identified, the basis risk can then be quantified and communicated. Once quantified and understood, the structure can then be tailored to modify the expectation as appropriate.

Let’s examine some typical methods for quantification of basis risk in two types of parametric structure. Pure parametric, in which a measured parameter is used to proxy the loss, and a simple modeled loss structure, where a modeled footprint is used with exposure, vulnerability, and financial models to create a modeled loss for the event.

Pure Parametric

A range of methods have been developed to assess basis risk in pure parametric structures, these can also be applied in modeled loss and indemnity cover.

To develop this idea, we will use a theoretical example of a parametric wind trigger in which there is a linear payout based on the wind speed measured at a single location.

Following the previous definition of basis risk, the expectation with this structure is that wind speed during an event correlates with total loss. Conveniently, it is possible to use catastrophe models to uncover this correlation.

Each point in Figure 1 represents a stochastic event, with its associated modeled loss and modeled wind speed at the measurement location.

Figure 1: Hazard against modeled lossThe form follows that of the vulnerability of the underlying exposure. The function that describes this relationship is contained within the index formula, which is used in combination with an exposure weight to transform the wind speed to an index loss. The results of this transformation of hazard to index loss are displayed in a basis risk plot (Figure 2):

Figure 2: Basis risk plotThe correlation between the two variables is one measure of the overall basis risk. However, basis risk is a two-sided coin, it has positive and negative components, termed as overpayment and shortfall.

Overpayment describes the situation in which the payout from a structure is greater than the loss experienced during an event, whereas shortfall describes the more important situation for the risk holder, in which the payout is less than the loss.

It is more insightful to measure basis risk with respect to a target layer. Overpayment and shortfall can then be measured as a percentage of the total layer width. Figure 3 displays regions of shortfall and overpayment with respect to a target indemnity layer of 200 XS 200, for the same events as displayed in Figures 1 and 2.

Figure 3: Shortfall and overpayment with respect to a target indemnity layerThe degree of shortfall or overpayment can then be calculated. The following formulae are commonly used to calculate the basis risk for parametric structures with a linear payout.

We can calculate these basis risk metrics for all stochastic events, and produce conditional probability plots which describe the expected degree of overpayment or shortfall. Shortfall is conditional on an event exceeding an indemnity attachment, and conversely overpayment is conditional on an event attaching on the index side.

Shortfall and overpayment can be further quantified and visualized using conditional probability plots. Figure 4 displays the probability shortfall or overpayment of exceeding a range of thresholds. As can be implied from Figure 3, and quantified in Figure 4, the example structure shows a moderate bias towards shortfall.

Figure 4: Conditional probability plotUsing these methods, it is possible to understand and communicate the basis risk associated with the structure. This helps to refine the trigger mechanisms to a point where all stakeholders are comfortable with the levels of associated basis risk.

It is important to note that while hazard and loss uncertainty can and should also be factored in, we should remember that basis risk metrics calculated within a model cannot account for all the uncertainty that exists. Indeed, basis risk can be most well understood if measured using independent models and methods.

Minimizing Parametric Basis Risk

Once quantified, there are ways to close the gap between the expectation and outcome. The simplest of these is to change the attachment level.

If the expectation from a risk holder is that a payout should be received after any event that makes the news, then the index attachment level can be lowered, and the trigger can be biased towards overpayment. This transfer of basis risk from shortfall to overpayment comes at the cost of a higher premium.

A less costly option may be to introduce a phased attachment, where there is a small binary payout at a lower attachment threshold, with the remaining principal more closely tied to an indemnity layer. This stepped payout mechanism may help to manage the reputational risk associated with a binary parametric trigger structure.

A more technical approach to reducing basis risk requires a more detailed understanding of the sources of uncertainty. Within the confines of the model, the overall basis risk in pure parametric structures primarily derives from:

The displacement of the exposure from the measurement station(s)

The ability of the index formula to capture the vulnerabilities of the exposure

One way to reduce the basis risk is to increase the number of measurement stations, and assign exposure to the station which best proxies the hazard at the exposure. Another is to use more index formulae to better capture the range of vulnerabilities.

Modeled Loss

The obvious extension is that a simple modeled loss based trigger solves both of these problems, where we effectively know the hazard at all locations, and can use the true vulnerabilities of the exposure. Surely this reduces the basis risk to zero?

Not necessarily. The primary sources of uncertainty in a modeled loss trigger are often distinct from those in pure parametric. The nature of the uncertainty is also more structure specific, making it difficult to generalize the drivers of basis risk in “modeled loss”. For example, in different forms of modeled loss triggers, the process used to generate the modeled hazard footprint, or the development of loss curves from limited historical data might drive basis risk in a modeled loss trigger.

The example of modeled loss draws out an important feature of basis risk; some sources of uncertainty can be quantified easily using models, and some cannot. A model is well placed to quantify the correlation between hazard and loss in a pure parametric structure, but less well equipped to convey the uncertainty that exists within itself, which can be relatively more significant in a modeled loss structure.

In light of this, when assessing basis risk in modeled loss triggers we need step outside the confines of the model at hand, and assess the structure independently using external models and the real world. A daunting task, with project resources and the historical record often restricting the insight that can be gained, though one which can greatly enhance the success of the structure.

On What Basis

Importantly, and somewhat contrary to common perception, both modeled and un-modeled sources of basis risk exist in all structures. The balance between the two shifts depending on the dominant driver of uncertainty, be it within pure parametric, modeled loss, or indemnity. In all cases, identification, quantification, and communication are the keys to understanding basis risk.

The benefits of a clear understanding of the basis risk are well worth the effort in attaining it. Structural decisions can be made with greater confidence, potential options can be measured against one another, and the expectation that a structure always pays out when there is a loss can be set appropriately.

Ultimately, the potential for surprises is reduced with greater understanding, and the risk transfer is more likely to function as expected. Basis risk can never be entirely eradicated, though with the right analytical approaches it becomes much more manageable.…

Conor is a senior consultant in the Capital and Resilience Solutions team in London. He works on a broad range of catastrophe bond transactions, and has particular experience in modeling parametric structures, leading on recent innovative transactions including MetroCat Re Ltd. 2017-1.

Additionally, Conor researches the application of catastrophe models to public sector resilience initiatives. This includes modeling critical urban infrastructure in Mexico for 100 Resilient Cities, modeling linear transport networks in coastal U.S. states, and working with the U.K. Department for International Development to assess the suitability of a catastrophe risk pool in Asia.

Conor holds a masters in Natural Sciences from the University of Cambridge.