On May 1, 2016, a small wildfire was spotted some 4 miles (7 kilometers) southwest of Fort McMurray. With a population of around 66,000, Fort McMurray is renowned in Canada as an oil production center, located within the vast Athabasca oil sands across northeastern Alberta. An estimated 1.7 trillion barrels (equivalent) of bitumen lie under 54,000 square miles (140,000 square kilometers) of forest and peat bog.

Firefighters on the scene quickly acted to suppress the fire, but it reached Fort McMurray two days later as winds pushed embers into the town, causing an urban conflagration. More than 2,579 buildings were destroyed. The fire then grew to over 100,000 hectares in just four days, and nearly half a million hectares by May 17. It then burned for a further 15 months, and on August 2, 2017, the fire was finally extinguished. Nearly 600,000 hectares had burned.

Thanks to one of the largest evacuations in Canada’s history, some 88,000 residents safely left Fort McMurray. Two fatalities occurred as a result of a vehicle collision from the evacuation, but there were no other fatalities from the fire. The oil sands production facilities were largely protected from the fire, but production was disrupted.

Canada’s Most Costly Disaster

Fort McMurray was by far the most costly wildfire in Canada’s history, and the most costly disaster experienced by the country. The overall estimated financial impact according to Swiss Re, was CA$8.9 billion (US$7.13 billion) and insured losses totaled CA$1.7 billion (US$1.36 billion).

Canada is no stranger to wildfire. According to the Canadian Interagency Forest Fire Center, an average of around 2.93 million hectares has been consumed by wildfire annually over the last 10 years. Many fires burn in large, sparsely populated areas. Canada is the fourth-largest country in the world in terms of land area but has a population density of around four people per square kilometer. Because of the large area, suppression is difficult, and most fires in Canada are allowed to run their course. But a fast-spreading event threatening significant exposure, such as Fort McMurray can quickly strain suppression efforts and become uncontainable.

If a wildfire can produce Canada’s largest-ever insured loss, and as wildfire ranks second to flood in terms of overall insured loss, what does this mean for the insurance industry? There is a need for insurers to thoroughly analyze wildfire tail risk and its potential to impact urban areas and high-value industrial complexes. What can we learn from Fort McMurray and other significant Canada wildfires, and what can insurers do to understand and manage wildfire risk, such as in all-perils homeowner policies?

Conducive Conditions

Two key factors stand out from the Fort McMurray Fire. The first was that the climatic conditions since the previous winter were very conducive to wildfire, with low precipitation and higher-than-average temperatures, causing forest fuels to dry out. These conditions are not unusual; since 1994, nearly a quarter of fires in the Alberta province started in May. The fire spread accelerated on the first day; a report from consultants MNP stated that humidity levels had dropped quickly, the temperatures swelled to over 77 degrees Fahrenheit (25 degrees Celsius), and wind speeds increased. These conditions resulted in the fire rapidly growing, and embers picked up on strong winds started spotting properties in Fort McMurray on May 3.

The second key factor was that although many properties were destroyed or damaged, more than 90 percent of the structures in the affected area survived the fire. The homes that survived demonstrated that the structure and the immediate surrounding area were more resistant to fire ignition. Programs such as FireSmart Canada, and adherence to building codes had played their role in helping to protect individual structures.

Model Evolution

Although fire hazard models, zoning, and maps are used by the industry to assess and price wildfire risk, there is a need to accommodate all factors – from climatic conditions to the specifics of each structure. Risk modeling needs to show how a wildfire translates to on-the-ground damage and loss, and at a high-resolution level to understand how individual locations will be impacted.

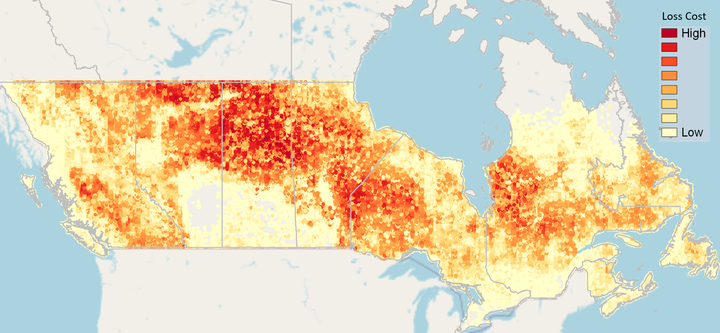

New risk modeling, with the launch of the RMS® Canada Wildfire HD Model, now offers this granular view (Figure 1). It provides coast-to-coast, probabilistic wildfire modeling for all 10 provinces – based on a simulation-based framework with millions of realizations across thousands of simulated years. Capturing topography, fuel type, and weather parameters, the new model includes ignition and spread, in addition to ember footprints, smoke footprints, and urban conflagration.

Figure 1: Canada map showing wildfire loss cost hot spots using the RMS Canada Wildfire HD Model

Events such as Fort McMurray, Alberta’s Slave Lake Fire in 2011, and the Okanagan Fire in British Columbia in 2003 – all urban conflagration events, can challenge solvency and point to the need to drill down into wildfire risk especially for wildland urban interface (WUI) areas. These “black swan,” long-tail scenarios, such as Fort McMurray, require analysis of potential risk accumulations, to provide reassurance to regulators, and must be managed through better risk selection and pricing. The RMS model helps to identify future major urban conflagration events with analysis of structure-to-structure ignitions. It also accounts for the contribution of damage from embers, and losses from smoke damage.

Knowing the wildfire risk of an individual location is proving to be a game changer for the insurance industry. To help achieve this, the new RMS model gets to the 50-meter-resolution level, allowing accurate risk selection and pricing. Mitigation measures, which certainly made a difference for Fort McMurray, are accommodated in the model.

Initiatives in Fort McMurray and across other WUI areas are helping to improve wildfire resilience. But with growing exposure in these areas, the balance is tipped toward a worsening outlook – the influence of climate-change factors such as longer spring and summer seasons with warmer, drier conditions, and consequences for fuel growth and ignition. With new modeling, the industry can benefit from the most comprehensive, fully probabilistic view of wildfire risk for confidence in risk selection and growth opportunities, while supporting and promoting policyholders’ efforts to improve wildfire resilience.

Vice President, Model Product Management, Moody's RMS

Michael leads a team that establishes requirements and features for all of the Moody's RMS North and South America climate models. Michael's responsibilities include overseeing the submission of Moody's RMS products to regulatory reviewers, such as the Florida Commission on Hurricane Loss Projection Methodology (FCHLMP).

Michael has led studies of insurance mitigation programs for the state of Florida, as well as the World Bank. In his past 14 years at Moody's RMS, Michael has also worked as a lead wind vulnerability engineer, a director of claims and exposure development, and as the head of the mitigation practice. He has worked in commercial wind-tunnel laboratories doing studies on wind loads for a variety of buildings.

Before joining Moody's RMS, he was involved in the development of Federal Emergency Management Agency (FEMA) HAZUS-MH software for hurricane risk assessment, and he taught courses on the use of HAZUS hurricane and flood components. Michael has also led studies on mitigation cost effectiveness for building codes such as the 2001 Florida Building Code and the North Carolina Building Code.

Michael holds a bachelor's degree in Civil Engineering and a master's degree from the University of Western Ontario in Canada in Wind Engineering.