Understanding and projecting future mortality requires consideration of the widest set of relevant risk drivers, or a view of risk could be compromised. (Re)insurers rely primarily on actuarial models to determine future risk, but models based on the historical record do not fully represent the risk landscape. These models can also make it very difficult to decipher drivers of emerging trends in mortality rates in a data-driven manner, as the drivers tend to be complex and interconnected.

Changes in mortality arise from many different causes. Distinct phases of social change can be identified in the historical mortality record and literature. Shifts from one regime of mortality improvement to another happen as scientific advances (new treatments), economic conditions (financial crisis), and social acceptance (reduction in smoking) combine to create new conditions.

Over time, the primary drivers of mortality improvement have changed. So too, have the most prevalent causes of death. Consequently, (re)insurers can expect:

Each phase to be associated with a particular average improvement trend

Each phase to have its own characteristic level of volatility

Diversification between phases

In estimating the trajectory and distribution of future mortality rates, (re)insurers should expect that these characteristics would also apply to future phases of improvement.

Applying a Probabilistic Approach to Understanding Mortality Risk

The RMS® Longevity Risk Model takes a different approach from actuarial methods. Our model embraces the medical science specific to longevity risk called “geroscience,” which is the study of the interface between aging and age-related diseases. It establishes the interdisciplinary scientific foundation for longevity risk, covering fields ranging from molecular genetics and chemical biology to bioinformatics. The modeling recognizes that with all medical science, the path of geroscience advancement is not deterministically predictable; rather, it is inherently a stochastic process.

In essence, RMS quantifies future mortality risk by blending medical science and best-in-class statistical and actuarial techniques. This involves coupling current mortality trajectories with structural models of the underlying drivers of mortality improvement to refine the uncertainty around future mortality projections. This modeling approach has helped insurers and pension schemes better understand the underlying drivers of future mortality, allowing a more meaningful view of the risk that is critical to making business decisions.

The release of the latest RMS Longevity Risk Model, running on the cloud-based RMS LifeRisks® Version 2.8.1 software platform, now represents a major step to fully understand the complexity of the risk landscape. All of the updated Longevity Risk Models (U.S., Canada, and the U.K.) incorporate the latest available death, population, and market biometric data, and they allow for customized, user-defined views of risk to drill down into each risk driver to help price risk more effectively.

New Modeling Framework Offers the Most Realistic View of Risk

The new longevity model framework is truly holistic and forward looking. Built from the ground up, the framework recognizes that future mortality is informed not only by the historical mortality record but also on available knowledge of possible future developments affecting mortality. The new framework enables modelers to seamlessly examine both a new short-term view as well as the long-term trajectory and stochastic process.

This, in effect, makes the RMS Longevity Risk Model a hybrid model, allowing for modelers to take the best characteristics of both actuarial and stochastic modeling. The model incorporates the most recent societal trends while overlaying medically informed intuitive parameters that place realistic constraints on the timing and efficacy of “vitagions,” future drivers of mortality improvement. Combined, this provides a model that better predicts risk in the decades ahead.

In order to effectively incorporate both an actuarial approach and new trends, the model requires a robust set of vitagions that will produce a more diverse range of mortality trajectories. To address these needs, RMS models the following vitagions to build a comprehensive view of risk:

Lifestyle: Nine individual risk factors that affect health, such as smoking and obesity

Medical Intervention: New medical treatments, including pharmaceuticals, biologics and vaccines, improvements in diagnostics, surgical techniques, and the delivery of new or existing treatments

Health Environment: Hygiene, sanitation, pollution, knowledge and awareness of health issues, access to health care, health and safety legislation, and other economic factors

Regenerative Medicine: Techniques for repairing and renewing cells and organs, including stem cell therapy and nanomedicine

Anti-aging Processes: Discoveries that directly affect the human aging process and may decrease an individual’s effective biological age below actual chronological age

Finally, to supplement and contextualize the stochastic Longevity Risk Model results, RMS has developed a suite of deterministic scenarios, which include the RMS reference view (best estimate), risk factor-driven scenarios (e.g., alternative smoking or obesity trajectories), medically informed cause-of-death scenarios, and economic scenarios. Consideration is explicitly given to COVID-19 mortality data in the statistical calibration for the short-term trend.

Using a Short- and Long-Term View to Improve Risk Pricing

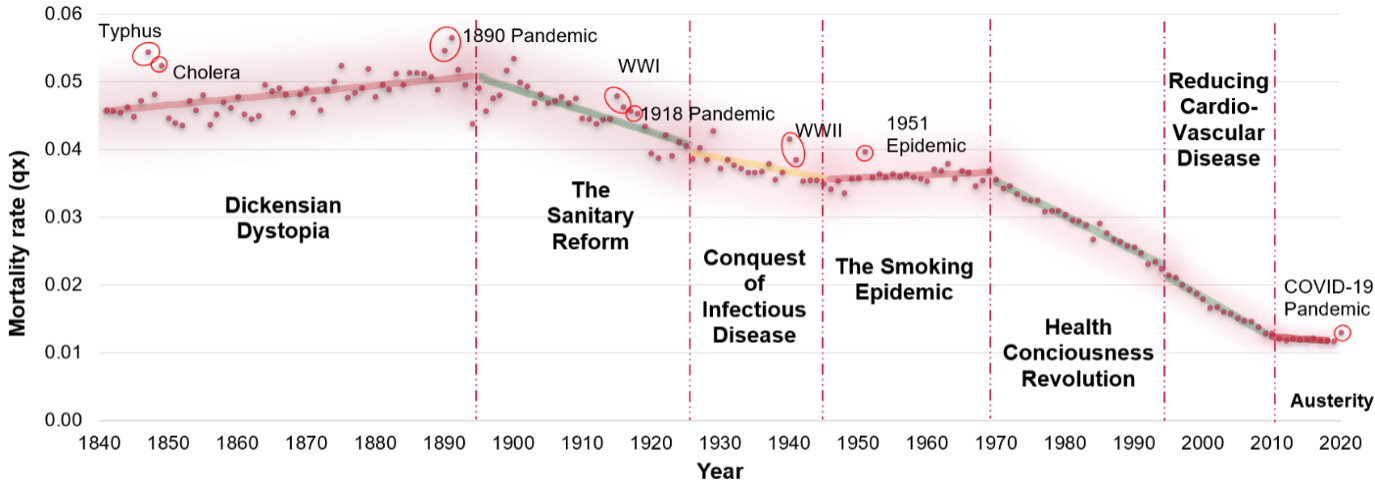

Why should (re)insurers incorporate a shorter-term view of risk into long-term mortality trends? Mortality rates have changed at different rates during different historical periods. Figure 1 shows the historical mortality rates of 65-year-old males in England and Wales over the past 180 years.

Figure 1: Mortality improvement milestones over the past 180 years: historical mortality rates for 65-year-old U.K. males and broad phases of social change (Source: Office for National Statistics)

Over short durations, observed mortality trends can run above or below the longer-run trends. A period of high mortality improvement may be caused by a burst of progress generated by medical innovation that is rapidly disseminated among the population. This may be followed by a period of relatively lower improvement as the beneficial impact of such techniques is fully realized. This effect can be seen in the historical mortality records across multiple western countries, such as the U.S and Canada.

It is important to distinguish between periods of higher mortality improvements, in which causal interventions will have a biological limit (e.g., effect of statins on cardiovascular disease). Equally, it is important to identify a period of below-average improvements (e.g., economic stagnation), where the cause may be reversible or responsive in the future to medical or social intervention.

The updated RMS Longevity Risk Model now provides additional flexibility to reflect recent trends or a trend dynamic. Prevailing rates have fallen sufficiently to justify adding a durational element to the projection. This addition enables the model to reflect both short-duration trends and avoid suppressing improvement rates at medium- and longer-term durations.

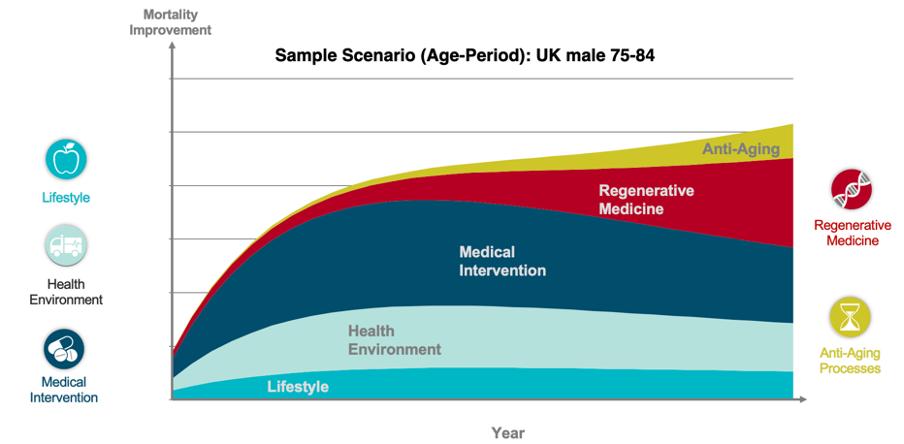

This update significantly improves the predictive power of the model, enabling it to produce trajectories that exhibit waves consistent with what has been observed in the historical record, while better fitting in the short term to the prevailing trend. Figure 2 illustrates a sample projection scenario for each vitagion. However, each scenario can differ dramatically depending on the stochastic sample within each vitagion.

Figure 2: Sample scenarios for 75-to-84-year-old U.K. males, by vitagions (Source: RMS UK Longevity Risk Model)

Additional Model Updates

RMS has also invested in several additional new and innovative capabilities for the RMS Longevity Risk Model, including:

Bottom-up Bayesian modeling of individual biometric risk factors (e.g., smoking) to quantify the trajectories and uncertainty associated with the lifestyle vitagion

Enhanced age granularity to provide a more detailed quantification of longevity risk, driven by differences in risk factors and underlying causes of death

Refinements to the temporal stochastic process to allow for better estimation of the risk over various durations

Updates to the vitagion trend decomposition to better refine risk associated with each vitagion, embedding the new Bayesian approach for lifestyle

New COVID-19 deterministic scenarios to help (re)insurers estimate the potential impact of the pandemic on future mortality improvements (e.g. application of m-RNA technology)

Embedding the latest cause-of-death mortality data

General software improvements including the ability for clients to embed their own short- and long-term views using the LifeRisks model editor tool

Combined with the new model framework, these updates provide a more diverse range of mortality trajectories and therefore a richer loss distribution, improving the predictive power of the model. They also provide a more refined view of the risk associated with the demographic profile of the portfolio.

To learn more about the new model updates or to get more information on our suite of mortality risk solutions, check out the new LifeRisks brochure. You can also speak directly with a LifeRisks specialist through the contact us page.

Share:

You May Also Like

Ashley Campbell

Consulting Actuary

Ashley is a qualified Actuary with 10 years’ experience working in the life insurance and pensions industry. He has worked with some of the largest life insurers and pension schemes in the U.K. across a breadth of areas such as risk management, risk transfer, capital modeling and solvency II. Most recently he has been focused on longevity and pandemic risk modeling, and regularly presents on these topics to the actuarial and insurance community.