Factors such as factory closures due to COVID-19 lockdowns, higher energy prices due to the impact of Russia’s invasion of Ukraine, shipping container shortages, congestion at ports, and intermittent spikes in demand have disrupted supply chains globally and led to above-normal general inflation trends in many countries.

For the construction industry, a focus area for property and casualty insurers, a combination of sustained demand and supply chain constraints, together with rising energy costs have led to price escalations and lead time increases not seen in decades.

As supply chains come back to life and energy prices start to look for a new equilibrium, RMS continues to further its research into the macroeconomic data and trends driving the current environment of rising construction prices.

Construction Industry: Examining 2020-22 Inflationary Trends

The construction industry found itself in a unique and unprecedented situation during the early months of the COVID-19 pandemic, as production capacity decreased sharply due to the imposition of COVID-19 quarantine and social distancing measures.

But some economies then experienced a sudden increase in demand, as home renovation and new residential construction were fueled by the growth in remote working, low-interest rates, and high buying power within some income groups.

This strong and sustained demand for residential construction was experienced among developed economies including the United States, Australia, and Canada, and this increased demand, combined with logistical issues, then led to the 2020 global lumber price crisis.

Looking at 2023, lumber futures prices have now reduced significantly and are only slightly higher than pre-pandemic levels. But prices for wood products remain high.

This is due to higher transportation costs and unresolved supply chain issues, as port congestion, low warehouse availability, increases in warehouse construction costs, and early orders from companies trying to compensate for longer lead times, further contribute to supply chain disruption.

In the United States, the lead time for roofing materials and steel pipes has increased from 3-6 months pre-pandemic, to 9-12 months in 2022. Supply chain disruption is causing product scarcity which then leads to higher prices.

The Impact of Energy Prices

After the first few months of the 2020 global economic slowdown that initially led to low fuel prices, oil prices then started to increase again at the beginning of 2021, and then doubled in 2022.

High energy prices have impacted production and transportation costs almost globally. Steel, which is energy intensive to produce, has more than doubled in price – due to these high energy costs and production slowdowns, leading to higher construction costs in the nonresidential sector.

Gasoline and diesel prices have directly impacted contractors’ budgets by making it more expensive to bring materials to the construction site and to run heavy equipment such as bulldozers, concrete mixers, and cranes. Some major economies such as France and Japan which implemented early measures to cap gasoline and diesel prices did see lower inflation levels than their neighbors.

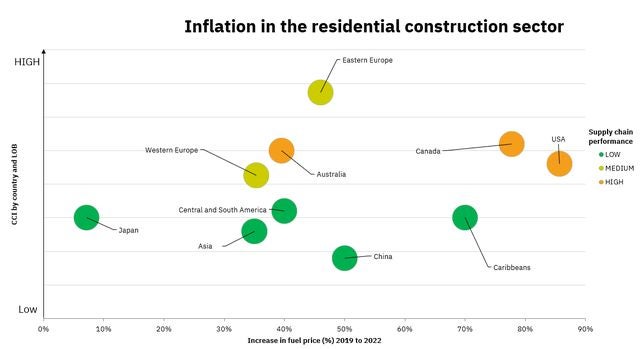

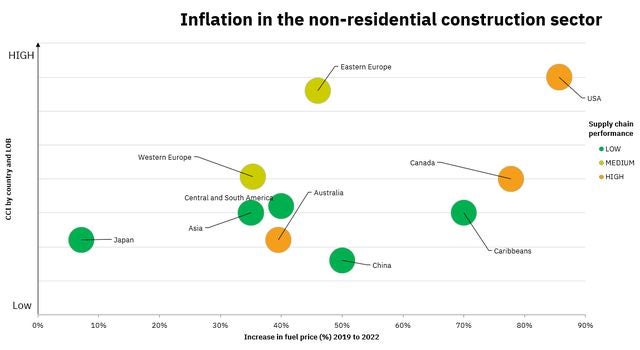

The following figure exhibits the inflation factors of several countries or groups of countries (y-axis) by peak increase in fuel price (x-axis) and Moody’s RMS view on supply chain performance (bubble size and color). Malaysia, South Korea, the Philippines, and Indonesia are combined into the Asia group.

The figure shows that lower inflation levels can generally be found in countries where the supply chain risk is lower; higher inflation levels can be found in countries with higher supply chain risk and higher energy increases. The supply chain risk is derived from Moody’s RMS analysis of the 2021 Container Port Performance Index report published by the World Bank.

Figure 1: Inflation in the residential construction industry by the change in energy price and supply chain performance. Source: RMSFigure 2: Inflation in the non-residential construction industry by the change in energy price and supply chain performance. Source: RMS

Where Are We Headed In 2023?

A lot of uncertainties still remain around oil prices, driven by factors including Russia’s invasion of Ukraine, OPEC oil production levels, and energy demand in Europe for the ongoing winter and upcoming spring. As a result, much of the inflationary drivers and impacts seen in 2022 will remain true for early 2023, but more significant changes can be expected later in the year.

While uncertainties in supply chain logistics remain high for commodities, such as cement, sand, concrete, iron ore, and lumber that typically require ocean, river, rail, or truck transport over long distances, trends indicate a positive outlook for transportation costs in 2023.

Lumber and steel prices experienced high volatility in 2020-22 and we may continue to see similar trends in the near future. However, core inflation is expected to closely follow energy prices. On the other hand, mechanical and electrical components, and complex manufactured products from Asia transported by containers will continue to have longer than usual lead times, resulting in locally high prices.

Port congestion has improved in 2022 but warehouse space is still limited in many countries, and warehouse-to-site transportation costs are still high. All these factors can impact residential and non-residential construction costs differently.

For insurers looking to quantify inflationary trends for their book of business, RMS has analyzed time series data to estimate bounds of inflation pertinent to residential and non-residential property exposures accounting for these underlying volatilities.

Clients can find more information about it on Moody's RMS Support Center via the whitepaper here and the inflation table here.

Getting the Measure of Inflation for the (Re)insurance Industry

…

Read More

Alex Martinez

Exposure Modeler, Model Development

Based in California, Alex joined RMS in 2021 after completing his doctorate. He is currently responsible for developing property exposures in Europe, and global marine cargo datasets. His recent research has focused on inflationary trends in the construction industry and their impact on global property exposures.

Alex holds a Diplôme d'ingénieur from the Ecole Centrale de Lille in France, a master’s in Environmental and Water Resources Engineering from the University of Texas at Austin, and a Ph.D. in Civil Engineering from the University of California, Irvine.