Taking Stock After the Impact of 1/1 Renewals on Primary Underwriting: What’s the Route to Long-Term Profitable Growth?

Evan CropperApril 14, 2023

Recent events have demonstrated that there has never been a more important time for insurers to reduce risk volatility and uncertainty in their risk decision-making processes.

The market is still picking up the pieces after the 1/1 renewals, which were described by broker Howden as representing “... the biggest reinsurance capital squeeze since 2008,” and saw a capital erosion of US$66 billion and reinsurance rates accelerate by more than 45 percent.

This has resulted in primary insurers paying much more to mitigate their books of business, leaving them with the difficult choice of potentially purchasing less reinsurance, paying more for it, or underwriting less in the upcoming year to maintain their current position.

Combine all this with high inflation and higher borrowing costs, and insurance chief risk officers (CROs) can expect difficult questions from their corporate boards on how they’re going to continue to grow when faced with challenging market conditions.

In this new risk paradigm, the feedback loop between underwriting, catastrophe modeling, and portfolio management must be tighter and faster. Business as usual won’t work anymore.

When underwriting guidelines are updated quarterly or even annually, portfolio managers make business decisions based on slow, cumbersome portfolio roll-ups. This leaves the business exposed to outsized cat losses, suboptimal portfolio diversification, slower growth, and potentially higher reinsurance costs.

If the goal of minimizing the uncertainty on how the entire risk organization manages the risk, then investments in underwriting systems should not be made in a vacuum. Decision-makers must invest in tools that deliver powerful and fast underwriting analytics as well as support how post-bind policies flow through the entire risk lifecycle.

Aligning the Corporate View of Risk in the Underwriting Process

Tightening and speeding up the feedback loop between catastrophe modeling and underwriting solutions is not easy. Currently, most systems use their own view of risk and utilize different financial models, hazard analytics, and even geocoding engines.

In fact, firms that purchase underwriting and catastrophe modeling solutions from the same vendor struggle with implementing a common view of risk between the two departments.

How does this drift between catastrophe modeling and underwriting systems from the same vendor happen? Here are three possibilities:

The catastrophe modeling and underwriting solutions may run on different exposure datasets.

Underwriters and catastrophe modelers may use different versions of the same model.

Tweaks to the catastrophe model that include the corporate view of risk may not carry over to the default view of risk used for underwriting.

With disparate systems and disparate views of risk, decision-makers are faced with several unattractive options on how to underwrite and model catastrophe risk.

The catastrophe modeling team can attempt to reconcile the different views of risk, which diverts resources away from value-generating activities and toward taxing data manipulation.

Underwriters can adjust pricing strategies to accommodate, which can result in lost business or underinsurance. Or cedant teams can transfer more risk to the reinsurance marketplace, which will eat into profitability.

Moody’s RMS™ built the UnderwriteIQ™ application to help firms reduce the uncertainty between how risk is underwritten and how it is transferred and retained across the risk lifecycle.

If you license both the UnderwriteIQ app and Risk Modeler™, our cloud-native catastrophe modeling application, you’ll see added benefits:

Both applications utilize the same portfolio of models and hazard analytics, meaning that both share the same underlying science and technology.

Both applications use the same exposure datasets and data enrichment services, ensuring that building characteristics that can have an outsized impact on losses (such as building composition for earthquake or the presence of basements for flood) are included in loss analysis.

Risk Modeler enables catastrophe modelers to apply their corporate view of risk to the underwriting workflow, so both teams are using the same approach to select and price risks.

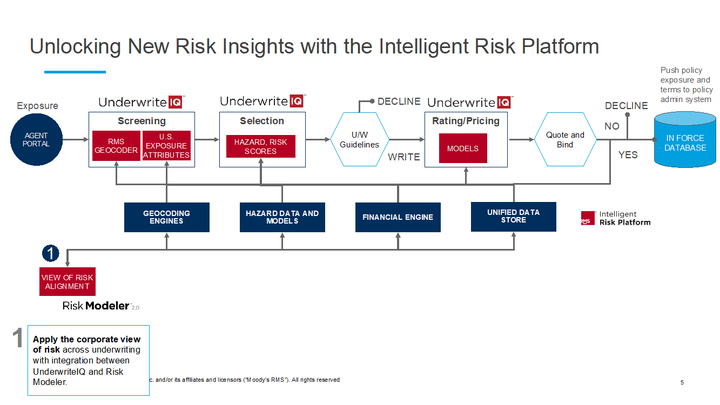

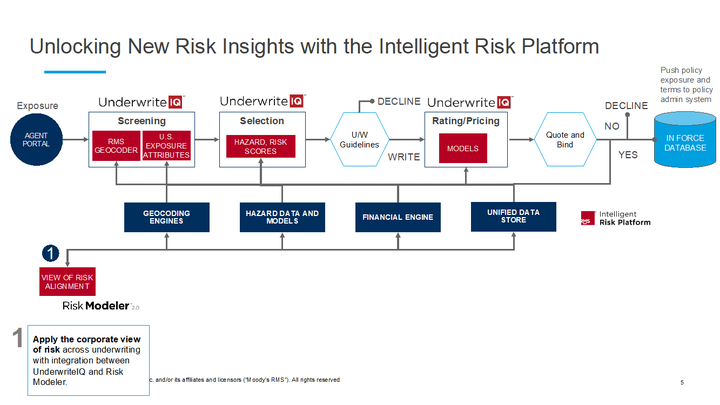

Together, these capabilities can create much greater consistency between the underwriting and catastrophe modeling teams (Figure 1). As a result, firms find it much easier to make portfolio diversification or risk transfer decisions of post-bind risks.

Figure 1: UnderwriteIQ and Risk Modeler applications expedite the corporate view of risk across underwriting.

Improving the Feedback Loop between Portfolio Management and Underwriting

For most firms, the period between underwriting post-bind policies and rolling up risks into the portfolio management workflow can take weeks, months, or even quarters.

Collecting hundreds of policies across multiple teams of underwriters using Excel spreadsheets – in addition to reconciling different formatting and combining with the existing portfolio of risks – is not only time-consuming but also brings the risk of user error to the underwriting and portfolio management process.

These technology limitations often result in the tail (the technology) wagging the dog (the risk organization). Because the technology can’t deliver a comprehensive and current view of the portfolio, firms adapt their organizational structures and decision-making processes to accommodate these limitations.

Instead of exposure managers and underwriters collaborating with each other, decision-making gravitates to the risk C-suite. When this happens, underwriting guidelines and portfolio steering decisions are made less frequently, tend to have a bigger impact on the day-to-day business, and are potentially based on outdated views of risk.

With the UnderwriteIQ and Risk Modeler applications plus ExposureIQ™, our cloud-native exposure management application, post-bind policies become immediately available in the Moody’s RMS Unified Data Store, which includes exposure characteristics and a real-time view of the portfolio, on the Moody’s RMS Intelligent Risk Platform™.

The UnderwriteIQ, Risk Modeler, and ExposureIQ applications all run on our Unified Data Store. Rather than having to complete several manual steps to add a single policy to the portfolio, exposure managers can intelligently schedule, on a daily basis, the execution of the portfolio roll-up workflow, incorporate complex treaty structures into their analysis, and conduct what-if scenario analysis on a live portfolio.

Portfolio management and underwriting teams can work together much more effectively on portfolio steering, underwriting, and risk transfer decisions because all three applications share a common view of risk (Figure 2).

Figure 2: UnderwriteIQ, Risk Modeler, and ExposureIQ applications join forces to facilitate portfolio steering, underwriting, and risk transfer decisions.

Following a hardening of the reinsurance marketplace, all key decision-makers across the risk life cycle will likely face greater scrutiny. Underwriters will not be an exception.

Underwriting speed and quality will certainly continue to drive growth. But if firms can reduce the volatility between their underwriting and other key disciplines, such as capital and cedant management, then it will have an outsized impact in the marketplace – which is still responding to the role of climate change on near-term catastrophe losses, higher borrowing costs, and higher reinsurance premiums.

By utilizing an underwriting solution that leverages industry-leading science and technology – and seamlessly collaborates with other applications hosted on Moody’s RMS Intelligent Risk Platform – decision-makers will be confident in the underwriting process as well as downstream responsibilities.

The upshot? Having the necessary support in place to best navigate these more difficult conditions.

Evan leads climate change and modeling product marketing for Moody's, where he helps customers develop more data-driven strategies using physical risk analytics. He has extensive experience scaling technology in the digital enterprise with a passion for using data to deliver better business outcomes.

Previously, Evan worked in various product management and marketing roles with Hitachi Vantara, Current - a subsidiary of GE Digital, and Cisco.

He holds a bachelor's degree in Political Science from Emory University and an MBA from Vanderbilt University’s Owen Graduate School of Business.