However, disclosures of Insurance-Associated Emissions have taken time to work through, a third of the 29 initial insurance industry signatories to PCAF itself have disclosed their IAE and few have explicitly committed to net-zero underwriting.

So what’s holding insurers back from disclosing their IAE? This could be a reflection of two broad themes:

The lack of a regulatory push (for now)

The challenge of sourcing the required data

Navigating a Diverse IAE Reporting Landscape

(Re)insurers find they navigate an array of complex regulatory demands that vary based on their underwriting portfolios; with IAE, the movement toward reporting is in its early stages, as regulatory bodies worldwide are still shaping their reporting guidelines.

A recent global survey revealedvarying degrees of regulatory development in this area. Canada sets a precedent in IAE reporting through its Office of the Superintendent of Financial Institutions (OSFI), which mandates the inclusion of IAE in Scope 3 (downstream) emissions inventories for insurers.

OSFI stands out for urging Scope 3 disclosures and specifying that insurers are expected to use the PCAF standard or a comparable industry-accepted approach. This positions the PCAF standard as a significant benchmark in regulatory approaches to greenhouse gas reporting.

In the European Union (EU), the approach towards IAE disclosures is integrated into a broader sustainability reporting initiative – the Corporate Sustainability Reporting Directive.

Launched in 2023, the Directive mandates over 50,000 businesses operating within the EU to disclose their environmental and societal impacts. This directive encompasses Scope 3 (in addition to Scope 1 and 2) emissions reporting starting from the fiscal year 2024, though stops short of endorsing a specific standard like the PCAF for Scope 3 disclosures.

Despite this growing global trend towards enhanced sustainability and Scope 3 emissions transparency, some jurisdictions have yet to mandate such reporting. In the U.S. and the U.K., Scope 3 emissions disclosure remains a voluntary practice for companies.

Nevertheless, there is anticipation around the U.K. Financial Conduct Authority (FCA) potentially incorporating Scope 3 emissions into its Sustainability Disclosure Requirements (SDR), possibly by 2025, reflecting a gradual shift towards standardized reporting requirements.

Responding to IAE Data Challenge: How Insurers are Balancing Data Quality and Coverage

The limited availability of data for emissions disclosures is a well-known challenge, and the practice of measuring and disclosing GHG emissions is not widespread, particularly for SMEs that make up a significant proportion of an insurer’s underwriting portfolio.

Consequently, insurers are adopting various approaches to implement the PCAF standard, dependent on the availability and quality of GHG emissions data from their insured entities.

Generally, insurers have stuck to disclosing their Scope 3 IAE based on their customers’ Scope 1 and 2 emissions only, with limited inclusion of Scope 3 of insureds in the disclosures.

For those including Scope 3, estimates are often derived from economic intensity-based calculations, which are not regarded as high-quality as directly reported GHG emissions from the insured entities. The associated PCAF Data Quality Scores (DQS) for the reported IAE offer crucial insights and transparency for the market and regulators regarding the quality of their reporting. To improve data quality, insurers will often work with third-party data vendors.

It should be emphasized that not every insurer adopts this method, which underscores the flexibility in implementing the PCAF standard. Allianz uses only reported emissions data of their insureds for their disclosures and reports a lower (better) DQS than other insurers that have disclosed to date, but also covers significantly less of their underwriting portfolio.

One area of debate among insurers is PCAF’s approach to using company data rather than asset or project-level data in estimating IAE for commercial lines. In their 2023 disclosures, Allianz tackled this issue using a simple adaptation of the standard PCAF methodology. In calculating the IAE associated with policies that insured renewables projects or assets, Allianz applied a factor of 10 percent to the standard company-level IAE.

Another consequence of the early stages of IAE reporting is the potential for significant revisions to previously reported emissions figures. In 2024, the Fidelis Partnership (previously Fidelis MGU) restated their 2022 baseline PCAF-aligned IAE measurement after taking additional data and the latest premiums into account. They benefitted from increased coverage, but also reported an increase in IAE, rising from 1.2 million tCO2e to 3.5 million tCO2e.

The Dutch insurer a.s.r. also restated their 2022 PCAF-aligned IAE baseline after an update to the data, with the result being a reduction of their commercial lines IAE from 122,000 tCO2e to 47,000 tCO2e for the same coverage by premium.

These adjustments reflect a broader industry trend toward greater accuracy and transparency in reporting, underscoring the evolving nature of IAE reporting practices and improvements in data quality.

A Clearer Path to Greater IAE Disclosure

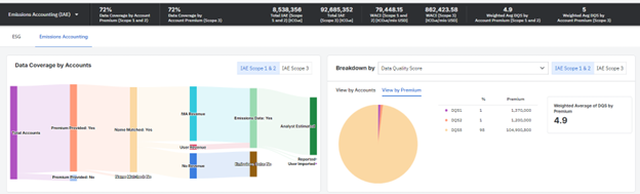

The industry is making positive steps towards Scope 3 insurance-associated emissions disclosures but there is still much work to be done. Moody’s is uniquely placed to support insurers with their Scope 3 GHG disclosures. We recently launched Moody’s Insurance-Associated Emissions Solution to help insurers implement the PCAF Insurance-Associated Emissions standard and respond more effectively to regulatory reporting requirements.

Figure 1: Moody's IAE Solution - Data Coverage by Accounts

Using ExposureIQ™, our cloud-native exposure management application on Moody’s Intelligent Risk Platform, the solution features emissions and revenue data for over 80 million companies, providing an extensive baseline of coverage for IAE emissions.

Contact us and find out more about how Moody’s can help with your Scope 3 reporting via our Insurance-Associated Emissions solution.

As part of Moody's insurance strategy team, Justin is one of the lead members in the research and development of Moody's Insurance Associated Emissions Solution. The solution enables insurers to measure the greenhouse gas (GHG) emissions associated with their underwriting portfolio in alignment with the PCAF GHG Reporting and Accounting Standard.

Justin has worked closely with the proof of concept (POC) and early adopter users of the solution, leveraging his expertise across data, modeling, and technology to support the delivery of the solution.

He has a doctorate in Physics with a specialism in statistical physics and stochastic models.

In 2016, Justin joined Moody’s working in the Economic Scenario Generator team supporting insurers with the use of stochastic models and scenarios for solvency capital reporting and financial asset risk management.