Five Years After Andreas: The Event That Changed the Severe Convective Storm Risk Landscape in Europe

Michèle LaiJuly 27, 2018

July 2013, and Central Europe was just recovering from severe floods during May and June when a series of severe convective storms surprised the (re)insurance industry. On July 28, hailstorm Andreas hit the Stuttgart region in southern Germany, causing widespread damage to property and automobiles. Andreas is also especially remembered as hailstorm Bernd hit the north of Germany the day before on July 27.

Overall, those two events caused approximately US$4 billion in insured losses to the (re)insurance industry. This was the highest insured loss during 2013, and the largest severe convective storm insured loss ever recorded in Europe; above Munich in 1984 (equivalent to US$5.4 billion overall and US$2.7 billion insured loss in today’s value) and Hilal in 2008 (US$1.5 billion insured).

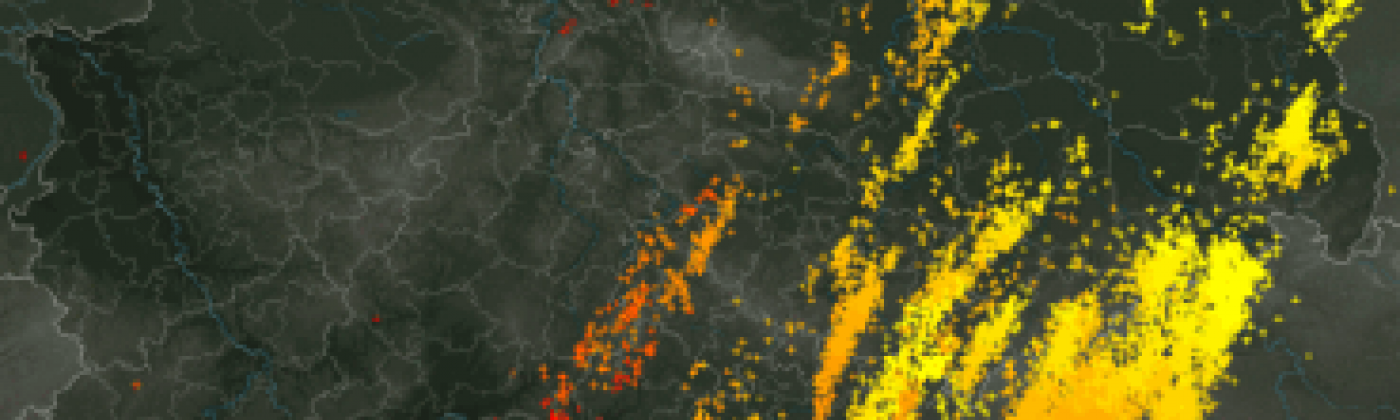

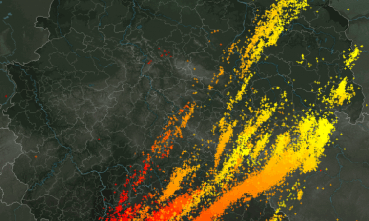

Figure 1: Lightning map during hailstorm Andreas. Source: Wikipedia / Lightningmaps.org

In addition to Andreas and Bernd, the 2013 severe convective storm season was continuously active in Germany and Europe, with some smaller but notable storms (Ernst, Manni and Norbert) that occurred throughout the season, leading to larger aggregate losses. However, that weekend of July 27-28, 2013 marked a turning point in the way the reinsurance industry considered risk due to severe convective storms in Europe. But five years on, what are the lessons learned?

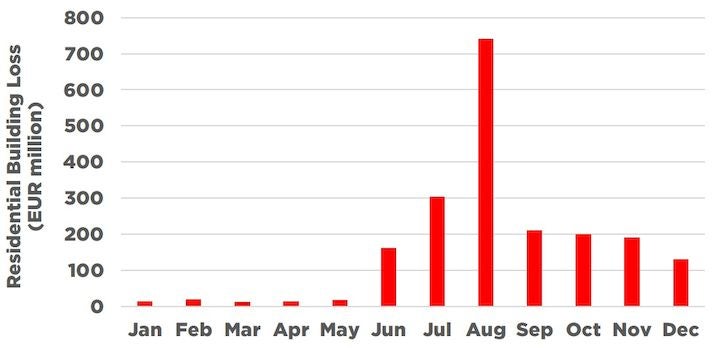

Figure 2: Reported insured losses for residential buildings in Germany during 2013. Because Bernd and Andreas occurred on the last weekend of July, losses for these two days were reported in August. Source: GDV

Severe Convective Storms Are Not Attritional and Aggregate to High Annual Losses

Andreas and Bernd highlighted the challenges that severe convective storms can present to the (re)insurance industry. After these events, it was clear that this peril should not be considered as attritional as it has been traditionally, it needed risk assessment through probabilistic modeling, similar to other perils such as windstorm or flood.

Additionally, insurance penetration rates are very high as severe convective storm losses are covered under wind policies in Europe, which made it even more imperative to be able to model this peril. And the following years only further confirmed the place of severe convective storm in the climate risk landscape, not only in Germany but throughout Europe:

2014: Ela (France, Belgium, Germany)

2015 and 2016: Hailstorms in the Netherlands

2017: Convective winds in Poland

The Challenges of Modeling Severe Convective Storm Risk

For effective hail and severe convective storm risk assessment in Europe, you need to understand that this peril poses several challenges for model development. Here is a (non-exhaustive) list of examples:

High-resolution and a Lack of Data

Severe convective storms are a very localized peril with a very steep hazard gradient, such as tornadoes which can be only a few meters wide. Even larger events such as derechos which can be larger than 400 kilometers (250 miles), present very inhomogeneous footprints with localized high intensity hazard streaks. This makes severe convective storms difficult to observe; the localized hazard might not be recorded by ground weather stations, so it is very difficult to observe and analyze the exact structure of the event footprint. Remote-sensing or radar data can help in this situation but are also not sufficient to get a full picture the event and answer questions, such as the size of hailstones that hit a specific location.

High-resolution and Smooth Climatology

Despite the high-resolution nature of the peril, the overall European climatology is relatively “smooth”. Larger risks can be seen along Europe’s mountain ranges, which provide the orographic lifting mechanism needed for the formation of thunderstorms, and smaller risks can be observed along coastal areas, which are dominated by a maritime climate. However, there are no sharp changes in the hazard pattern from one location to a neighboring location, as this can be the case in flood, where topography plays a crucial role.

Because of size of the events — as event footprints are rather small, a probabilistic model for severe convective storm requires millions of unique events to best represent the hazard. Given the localized nature of the hazard, a very high-resolution grid is needed to best represent the steep gradients within the footprints. This is computationally very expensive, which seems a bit contradictory when looking at the big picture: after all the climatology is very smooth. There is a requirement for a solution which can efficiently capture the high-resolution structure of event footprints, within a workable model.

Three Perils in One

There is a belief that severe convective storms simply equal hail in Europe. Indeed, hail is the dominant loss driver for most of the European countries, in short return periods as well as in the tail risk. However, straight-line winds also contribute significantly to the overall losses and should also be included in modeling. In some regions of Europe, straight-line wind can even dominate over hail risk. RMS will also include a tornado model in its new Europe Severe Convective Storm Models to provide a full picture. Also, read more about European tornadoes in my previous blog.

Hail Vulnerability is Changing Over Time

A catastrophe such as an earthquake or a windstorm acts as a trigger to build safer and more resilient buildings, meaning that the vulnerability of buildings usually improves over time. However, in the case of severe convective storms — especially with hail, vulnerability changes over time but not always in the right direction. An example of this is external insulation layers applied to modern buildings to improve energy efficiency. Compared to the traditional stone façades, they are more vulnerable to hail, and the same applies to aluminium roller blinds compared to wooden shutters.

Vehicles are Moving

Cars and other types of vehicles contribute to a significant proportion of the overall severe convective storm losses. In some events, more than 50 percent of the total losses come from automobile lines. It is therefore necessary to model these lines with more detail, which means:

More granularity in exposure coding, for example, differentiating private cars from trucks, cars in dealerships, commercial fleets, etc.

Account for the spatio-temporal component of vehicle exposure: depending on the time of the day, the locations and the number of exposed vehicles changes.

What Is an Event?

In a reinsurance contract, a severe convective storm event occurrence is often defined under the “hours clause”. A typical contract will state that a loss occurrence covers “…all storm, rain, hurricane, tornado, typhoon, cyclone and hail losses arising from one and the same atmospheric disturbance during a period of 72 consecutive hours”.

The definition of atmospheric disturbance is clear in the case of an extra-tropical cyclone or in a hurricane, because the atmospheric disturbance gets a name. This works well with these types of events which develop and mature over several days. However, thunderstorms can develop very quickly, but can also dissipate very rapidly. It is not unusual to have a supercell developing over a few hours, causing significant losses and then dissipating. In some cases, they will get a name, such as Andreas, which is often linked to the frontal system accompanying the thunderstorms. But in some other cases, they will not, especially when thunderstorms are occurring almost every day for one or two weeks. So, what is an atmospheric disturbance in the case of severe convective storms?

This question is more complicated that it seems, especially when it comes to applying reinsurance. Andreas and Bernd were two distinct events: two separate days, one in the north of Germany, and the other ones in the south of the country. However, five years later, the event is often referred as “Andreas” only and considered as one event (especially because of the hours clause).

This highlights the requirement for modeling hours clauses in a probabilistic model such as Europe Severe Convective Storm as the event definition defined by the modeler can have a big impact of the Occurrence Exceedance Probability (OEP) calculation.

Five Years Later…

RMS HailCalc is the first and only vendor hail modeling solution available in Europe, which covers eight countries, including Germany which was most affected by the series of thunderstorms in 2013. However, after the 2013 events, the (re)insurance industry and the cat modelers felt the need for a more sophisticated solution.

To respond to this demand, RMS is currently developing new Europe Severe Convective Storm Models, covering 17 countries in Europe, three perils and a new automobile model which accounts for the movement of vehicles. The models look to tackle many of the challenges mentioned and I look forward to sharing more details in future blog posts.

And five years after Andreas, it is always worth considering what are your lessons learned on European severe convective storms, and also look at how you and your organization work with this emerging and challenging peril.

Share:

You May Also Like

February 21, 2023

One Year Since Dudley, Eunice, and Franklin: Understanding Windstorm Clustering in Europe

Michèle joined RMS in 2013, and is based at the Moody's RMS Zurich office as part of the Global Climate Product Management team, focusing on European climatic hazard models. As part of her role, Michèle is the senior product manager for the new Moody's RMS Europe Windstorm HD Models and the Moody's RMS Europe Severe Convective Storm HD Models.

She holds a master’s degree in Atmospheric and Climate Science from ETH Zurich.