Streamlining Exposure Management: How Business Hierarchies in Moody’s RMS ExposureIQ Empowers Reinsurers to Mitigate Catastrophe Losses and Optimize Portfolios

Luke NormanJuly 04, 2023

With over a month now passed since the start of the current North Atlantic hurricane season, and with memories still fresh from the challenging round of reinsurance renewals at 1/1 in 2023, for reinsurers, significant potential stress is already stirring ahead of the 2024 New Year reinsurance purchases.

The reasons why the last 1/1 renewals in 2023 were particularly challenging for all concerned were a result of reinsurers dealing with tightening capital flows and a risk landscape shaped by growing natural catastrophe losses.

With insurers experiencing steep cost increases from rising inflation and the costs of Hurricane Ian, reinsurers tightened renewal timescales as they wanted to scrutinize what was coming onto their books, and to deeply analyze the risks they were taking on, so they could maximize their capital deployment.

To further tame the exposure they were taking on, reinsurers then sought to redraw the scope of the property catastrophe protection offered and used narrower coverage definitions, and excluded more perils, which can be seen as a blunt instrument to dampen down the risk.

Late Landfall: Complexities From Hurricane Ian

In addition, the uncertainty that many reinsurers faced over the potential catastrophe losses coming from events were further complicated as Hurricane Ian occurred late in the hurricane season making landfall in October 2022.

Reinsurers that were unable to quickly estimate losses across all cedants were left scrambling to assess their position right at the start of the 1/1 renewals.

Forced to reserve capital for these potential losses, reinsurers were then not able to fully capitalize on the potential of the 1/1 renewal period.

Therefore, given the potential impact of hurricanes on the industry, this time of year often brings a heightened sense of uncertainty, as events start to unfold.

An ability to quickly triage impacted cedants and to estimate their losses more accurately can help a reinsurer strengthen their financial stability and solvency position.

If they can’t do this, capital is tied up for the event, and they then need to underwrite more cautiously, impacting profitability.

Understanding the impact of hurricane losses for a single cedant – and a single line of business – may be easy to establish. The problem lies where a reinsurer wants to know the impact of losses across all cedants and to answer this question at speed.

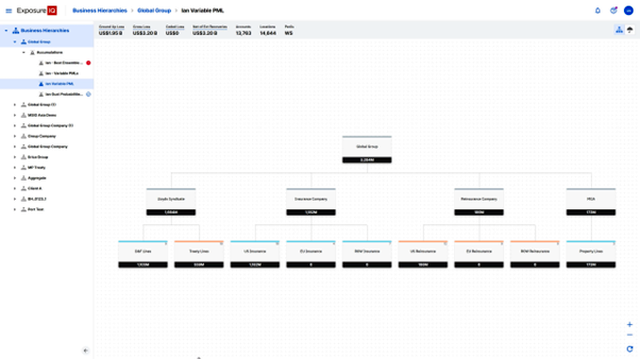

ExposureIQ is an application designed specifically for exposure management and with the new Business Hierarchies feature, this enables reinsurers to identify accumulations of risk across their entire company.

The import capability of ExposureIQ supports both Exposure Data Module (EDM) and spreadsheet imports, with support for CEDE and OED formats being added very shortly.

This enables reinsurers to centralize the exposure data from all their cedants, regardless of the data format.

With the ability to run billions of locations across thousands of cedants, for the first time reinsurers can now consolidate both insurance and reinsurance portfolios within a single application.

As an example, if a major hurricane strikes, reinsurers can use ExposureIQ Business Hierarchies to:

Quickly conduct pre-, during, and post-landfall event triage across an entire company to establish an early estimation of losses, and to drill down into the drivers of loss by a corporate entity, portfolio, cedant, or even a single location.

Gain insight into all outwards reinsurance recoveries for a true net reinsurance view of loss, allowing reinsurers to quickly understand the impact on their capital.

Utilizing the advanced analytics offered by Business Hierarchies, reinsurers can make informed, data-driven decisions to shape their underwriting strategy and minimize potential losses.

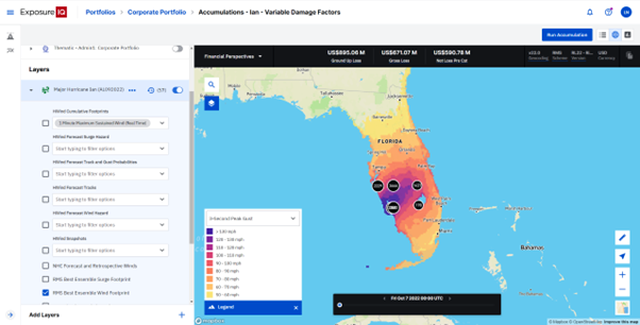

Figure 1: ExposureIQ: Viewing the impact of a hurricane event to identify affected cedants and portfolios.Figure 2: ExposureIQ: Viewing detailed losses for the highest contributing portfolio

Portfolio Differentiation

For the next 1/1 renewals in 2024, reinsurers also have the possibility to gain much-needed agility and to be able to better understand and accommodate their insurer’s growing need around portfolio differentiation.

Insurers are increasingly seeking to challenge broad risk assumptions from their reinsurers, by using relevant analytics to clearly make their case and explaining the nuances in their portfolios – and the nature of the reinsurance structures they are looking for.

Insurers believe that through clear, insightful analytics that can best explain the reality of their risk position, they have the best shot to get the pricing and coverage they need.

Moving from a broad-brush approach to shaping their portfolio toward a more differentiated insurance business, complementary to the rest of their company portfolio, insurers require sophisticated reinsurance structures to match.

And as more clients want the same differentiated approach, and layer in more and more structures, for the reinsurer, this then gets complex to manage – and the potential risk accumulation builds.

Using Business Hierarchies, reinsurers benefit from clear risk insights and can design advanced coverage structures that will meet their insurer client’s needs with ease, as well as the ability to:

Analyze each cedant’s exposure data in a granular way and identify cedants that increase the accumulation of risk in peak zones and cedants whose business has a diversifying effect on the rest of the company portfolio.

This analysis is important to give a tailored service to each individual cedant and ensures that the reinsurer is able to more effectively build a diversified portfolio that is complimentary to the rest of the underwritten business, enabling a reinsurer to:

Understand outward reinsurance recoveries and assess the effectiveness of their reinsurance program in a number of scenarios.

Promote greater risk transparency and communication from insurers with their reinsurers, by understanding more advanced analytics insights about their own exposures, providing the best opportunity to negotiate favorable terms with their reinsurers.

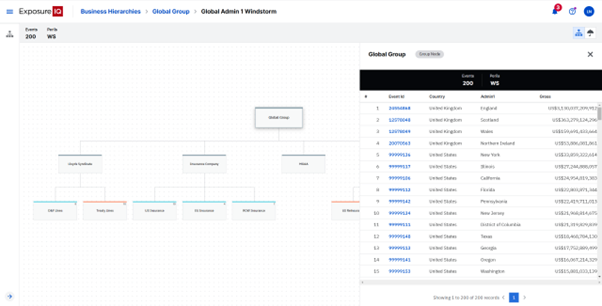

Figure 3: ExposureIQ: Identifying the top contributors of risk across the organization

The Business Hierarchies solution within the ExposureIQ application offers many powerful benefits for reinsurers, who want to easily monitor and manage risk accumulation across all cedants, get ahead of stability issues, and also to serve insurance clients more effectively if the coverage is triggered.

And with an eye on next year’s renewals, with a better understanding of each cedant and their reinsurance structures, how each structure works together with other cedants, and where the hotspots and opportunities lie, reinsurers can do the best they can, to accommodate their client’s needs, rather than having to resort to sweeping measures, squeezing coverage or dropping perils.

Streamlining Exposure Management: How Business Hierarchies in Moody’s RMS ExposureIQ Empowers Reinsurers to Mitigate Catastrophe Losses and Optimize Portfolios

…

Luke is a Director of Product Management at Moody's. He has more than 15 years of experience delivering risk management solutions to insurance and reinsurance companies. In his role at Moody's, Luke is responsible for developing the roadmap for Moody's ExposureIQ™, the company’s enterprise-class, cloud-based exposure management application.

Before joining Moody's, Luke was a Product Manager at AdvantageGo, managing the exposure management products Exact and Exact Max. Through this role, he has worked closely with clients across multiple insurance and reinsurance lines of business, to understand their exposure management needs and ensure they are met with innovative solutions.

Luke has a bachelor's degree in Mathematics from the University of Nottingham.