Hurricane Idalia: Strongest Hurricane on Record to Strike Florida’s ‘Big Bend’ Region

Callum HigginsSeptember 07, 2023

Major Hurricane Idalia made landfall as a Category 3 hurricane near Keaton Beach, Florida at around 11:45 UTC (07:45 local time) on Wednesday, August 30.

It is the first time that Taylor County, Florida, in the heart of Florida’s Big Bend region, has experienced a Category 3 hurricane or higher since records began in 1851.

In terms of the strongest hurricanes to strike Florida’s Big Bend region, Idalia has matched or surpassed the historical record. Idalia also became the eighth major hurricane to make landfall in the Gulf region since 2017.

Idalia’s Rapid Intensification

The storm rapidly intensified on August 29, the day prior to Idalia’s landfall, with wind speeds increasing by 45 miles per hour (72 kilometers per hour), fueled by the anomalously warm waters in the Gulf of Mexico.

As noted by Dr. Jeff Masters, Idalia is one of only ten historical storms since 1950 to intensify by at least 40 miles per hour (64 kilometers per hour) in the 24 hours before U.S. landfall. Five of these ten rapidly intensifying storms, all impacting the Gulf Coast, have now occurred in the past seven years.

Idalia’s rapid intensification had led the storm to briefly attain Category 4 status on its approach to Florida.

But a combination of dry-air entrainment and the beginning of an eyewall replacement cycle then weakened the system, seeing maximum sustained wind speeds falling to 125 miles per hour (201 kilometers per hour) prior to its center officially making landfall.

Nevertheless, Idalia is one of just 21 hurricanes known to strike Florida with winds at 125 miles per hour (201 kilometers per hour) or greater.

Following Hurricanes Irma, Michael, and Ian, Idalia is the fourth hurricane since 2017 to make landfall in Florida with winds equal to or exceeding 125 miles per hour.

Factors Modulating the Impact of the Storm

In a published loss estimate, Moody’s RMS estimated the total private market insured losses from Hurricane Idalia to be between US$3 billion and US$5 billion, with a best estimate of US$3.5 billion. This estimate represents insured losses associated with wind, storm surge, and precipitation-induced flooding.

In addition to the private insurance market, Moody’s RMS estimates around US$500 million in losses to the National Flood Insurance Program (NFIP) from this event, primarily in Florida.

Although this is a multi-billion-dollar loss event, despite the intensity, it looks as if a couple of crucial factors might have mitigated the extent of the impact of Hurricane Idalia.

First, is the landfall location, as the nine counties in the Big Bend region of Florida, including five coastal counties, have a significantly lower population and exposure density relative to much of the state.

Based on Moody’s RMS 2023 United States Hurricane Industry Exposure Database, the average total insured value for the counties of the Big Bend region is over 85 percent less than the average for all counties in Florida.

However, this lack of exposure is likely to be somewhat counteracted by the greater vulnerability of properties in the region.

The region has the lowest design wind speed of any coastal area covered in the Florida Building Code, set at peak three-second gusts of 130 miles per hour (209 kilometers per hour).

Additionally, according to Ian Giammanco at the Insurance Institute for Business and Home Safety (IBHS) over 50 percent of homes in the Big Bend counties were built in the eighties or nineties before the implementation of modern building codes. There are also almost as many mobile homes as single-family dwellings.

Properties with asphalt shingle roofs that are older than ten years are particularly likely to be susceptible to damage, even from wind speeds in the 90-100 miles per hour gust range, with any roof damage exacerbated by subsequent water intrusion.

The other mitigating factor is the relatively small wind field of Idalia, with a low radius to maximum winds (nine miles at landfall according to Moody’s RMS HWind) and the intensity of wind hazard rapidly declining outwards from this, reducing the spatial extent of the most damaging winds.

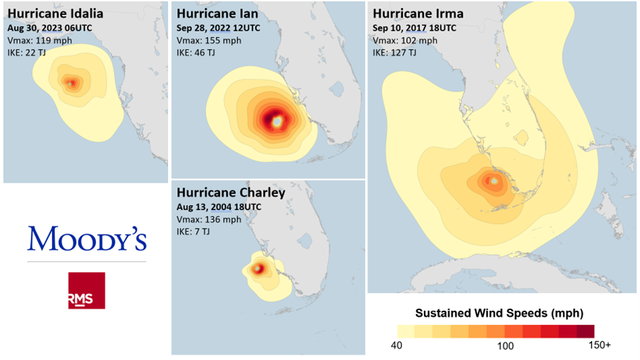

To put Idalia's wind field into perspective, we can compare it to several other Florida landfalling events: Hurricanes Ian (2022), Irma (2017), and Charley (2004).

Figure 1: Comparison of Moody’s RMS HWind snapshots (on the same scale) for Hurricanes Idalia, Ian, Irma, and Charley soon before landfall

By visually comparing Moody's RMS HWind snapshots for these storms, we can see that the wind hazard experienced from Idalia is much more akin to Charley than for Ian or Irma.

This is also reflected in their relative values of Integrated Kinetic Energy (IKE), a metric that conveys the intensity and size of a storm to gauge its potential destructiveness.

Of the four storms, Idalia’s IKE value at 22 terajoules (TJ) ranks third, with Charley the least intensive at 7 TJ, Ian (46 TJ), and Irma (127 TJ) substantially higher.

Catastrophic Storm Surge

Despite the overall size of Idalia’s wind field being relatively small, in some areas, it has resulted in record-breaking storm surge levels.

At a tidal gauge at Cedar Key, Florida, some 55 miles (88.5 kilometers) southeast of Idalia’s landfall location, a storm surge of 9.91 feet (3 meters) was reported, the highest on record going back to 1914.

The Gulf Coast of Florida is particularly susceptible to storm surge due to the bathymetry and topography along the coastline and storm surge elevation could have been significantly higher had the surge peak not coincided with low tide.

While storm surge is expected to be a significant driver of economic losses in Florida, insured losses are likely to be minimized by the low flood insurance take-up rates in the affected areas.

Most coastal counties hit by Idalia have National Flood Insurance Program (NFIP) take-up rates of less than 10 percent.

In terms of storm surge losses to the private insurance market (excluding NFIP), Moody’s RMS estimates these to be between 0.5 and 1.3 billion dollars, representing in the range of 15-25 percent of the total losses to the private insurance market.

Following landfall, Idalia delivered heavy rainfall and strong winds across Georgia and weakened as it tracked across the Carolinas where it brought dangerous storm surges.

Major coastal flooding was reported in Charleston and Edisto Beach, together with widespread areas of flash flooding.

Flooding in Georgia and the Carolinas will be exacerbated by the relatively saturated soil conditions, although away from the coast, flood insurance take-up rates in this region are in the single digits.

Moody’s RMS Response to Idalia

Moody’s RMS has been actively supporting its clients to respond to Idalia via the release of event summaries and accumulation and modeling information on the Support Center.

Additionally, customers using Moody's RMS ExposureIQ application have been able to take advantage of more frequently released and detailed accumulation layers available directly in the app.

In advance of Idalia's landfall, Moody's RMS HWind customers also received updated forecasts of industry losses four times daily, automatically delivered to their inbox.

The Moody’s RMS Event Response team has also issued a Private Insurance Loss Estimate, click here to read the full announcement, and please follow Moody’s RMS blog and social channels for further updates.

Callum is the product manager for Moody’s RMS Event Response Services (including HWind) and Agricultural Models and is based in London. Most recently he has been focused on improving client workflows through the integration of event response functionality within the Intelligent Risk Platform.

Previously, Callum has worked on climate change initiatives at Moody’s as well as the 2018 update to the Australia Cyclone Model.

Callum is a Certified Catastrophe Risk Analyst and holds an integrated master’s degree (MEarthSci) in Earth Sciences from Oxford University.